US dollar dominance and Asean currency prospects amid geopolitical shifts

A historical perspective and today’s debate

Many market participants view the early 1970s as the birth of modern foreign exchange markets, but history tells a different story.

While fixed exchange rates dominated the post-World War II era until the collapse of Bretton Woods, currency fluctuations had existed long before. As far back as the 1860 to 1870 period, the US dollar (USD) traded with notable volatility against the Swiss franc and British pound.

The 1915 to 1940 era was also marked by sharp currency swings.

Even in the ancient world, evidence of foreign exchange had existed, as Paul Einzig noted in “The History of Foreign Exchange.” He observed that when coins of both parties in transactions began to change hands by tale, a true foreign exchange system emerged.

Markets quoting foreign coins traded against each other likely developed during the fifth or sixth centuries BC and exchange rates between trusted coins gradually became standardized.

Einzig also remarked that the Roman aureus was the first currency to achieve global fame. Just as English is the “Latin” of today, the USD is the “aureus” of the modern era.

Thus, dollarization, the adoption of the USD as an official or de facto currency—became a defining feature of global finance.

Yet in recent years, the concept of dedollarization has gained momentum as countries seek to reduce dependency on the USD. This involves transitioning away from using the USD as the primary currency for trade, reserves and financial transactions.

Motivations include monetary independence, risk diversification and insulation from sanctions. In a postpandemic world shaped by risk management and resilience and amid heightened United States–China tensions, it is unsurprising that some nations are diversifying away from the USD, especially after US sanctions on Russia following the Ukraine invasion in 2022.

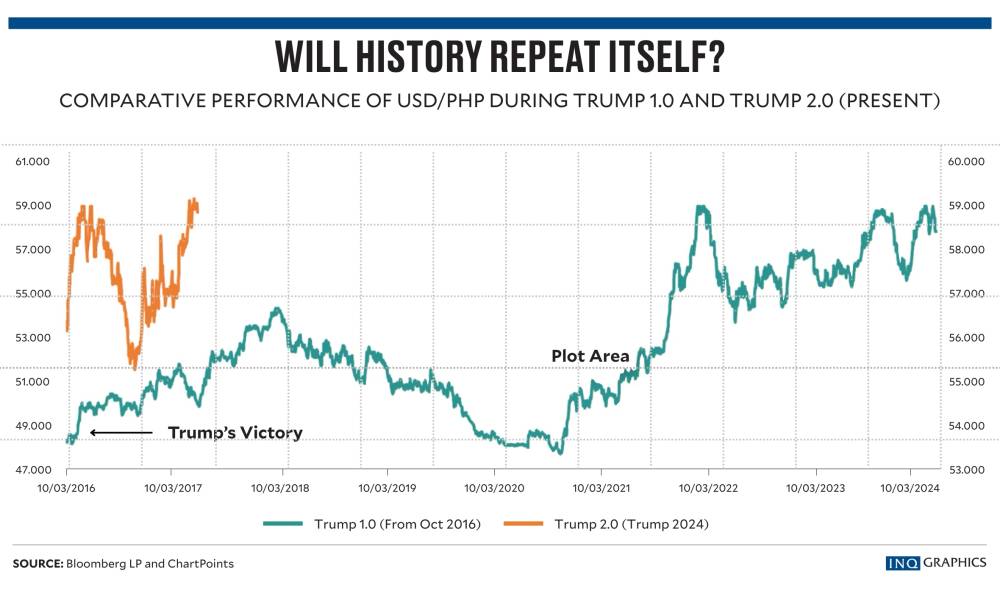

This article explores the prospects of dedollarization, the enduring dominance of the USD, and the outlook for Association of Southeast Asian Nations (Asean) currencies, particularly the Philippine peso—against a backdrop of Trump-era tariffs, rising geopolitical conflicts and regional security risks.

Dedollarization: Drivers, constraints and reality

The push toward dedollarization is driven by several factors.

First, sanctions risk has become a powerful motivator. US measures against Russia accelerated diversification into Chinese yuan and gold reserves by central banks seeking to avoid weaponized finance.

Second, tariff uncertainty under Trump’s trade policies has disrupted global supply chains, prompting some economies to settle trade in local currencies.

Third, technological alternatives such as central bank digital currencies and regional payment systems aim to bypass a dollar-centric infrastructure.

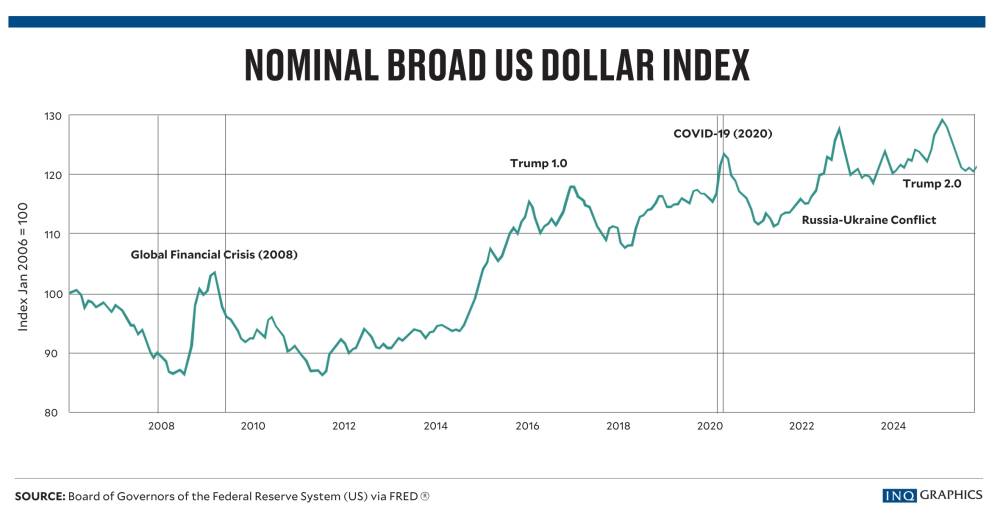

However, structural constraints remain formidable. Network effects are deeply entrenched: nearly two-thirds of global debt is dollar-denominated, and unwinding this dependency is a multidecade process.

Liquidity and convertibility advantages make the USD unrivaled for now while geopolitical fragmentation limits the scalability of initiatives led by BRICS. (BRICS is a group formed by 11 countries: Brazil, Russia, India, China, South Africa, Saudi Arabia, Egypt, United Arab Emirates, Ethiopia, Indonesia and Iran. It serves as a political and diplomatic coordination forum for countries from the global South.)

In short, dedollarization is real but gradual. The dollar’s dominance will persist through the next decade, though a multicurrency trade system may emerge by the 2030s.

Asean currency outlook: Navigating tariffs and trade realignment

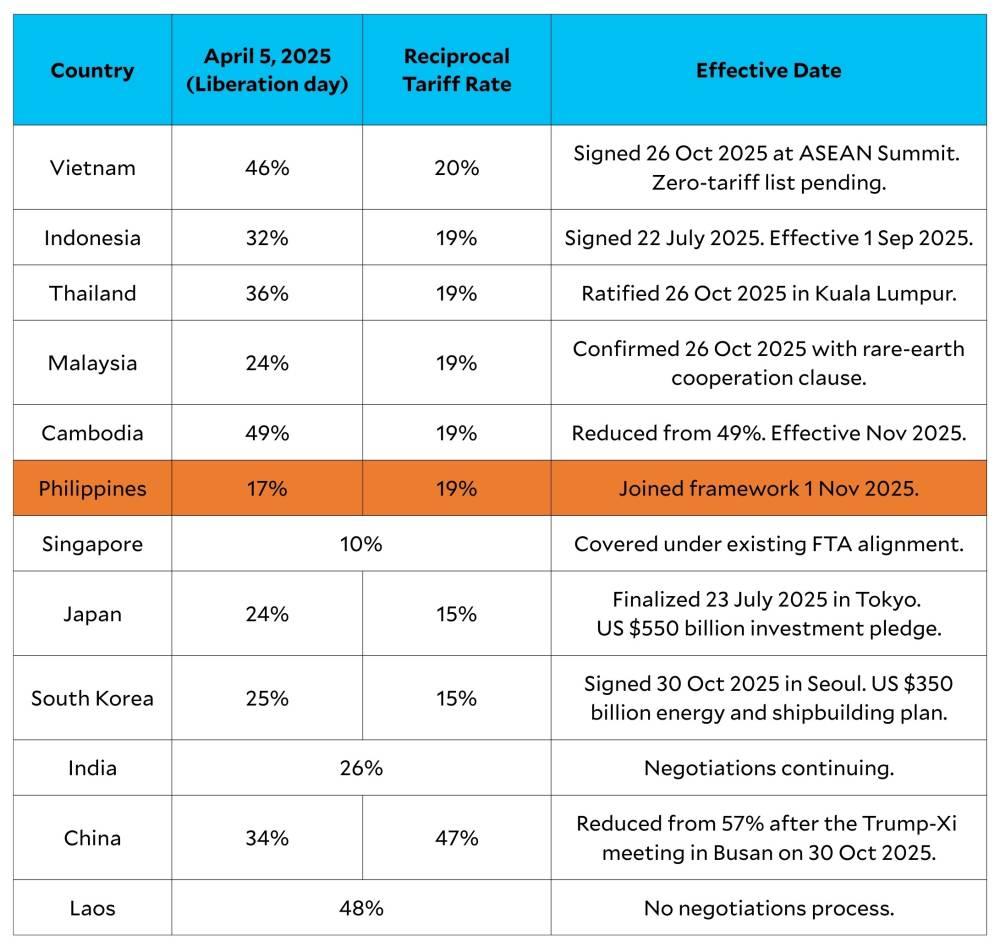

Asean economies enter 2026 with cautious optimism. Regional gross domestic product (GDP) growth is projected at 4.5 percent, slightly down from 4.8 percent in 2025, as US tariffs weigh on exports and private investment slows.

Inflation is expected to hover at around 2.1 percent, driven by food normalization and wage adjustments. Trade realignment is underway: regional commerce and foreign direct investments (FDIs) inflows are rising as firms bypass US-centric supply chains.

Currency performance will diverge. Low-yielders like the Singapore dollar (SGD) and Thai baht (THB) are likely to outperform, benefiting from safe-haven flows and strong external balances. High-yielders such as the Indonesian rupiah (IDR) and Philippine peso (PHP) face headwinds from tariff shocks and fiscal pressures.

The managed stability of the Chinese yuan (CNY) will anchor regional foreign exchange dynamics, especially for Vietnam and Malaysia.

However, Trump’s proposed tariffs, up to 40 percent on Asean exports, pose significant downside risks, particularly for electronics and textiles, which dominate regional trade baskets.

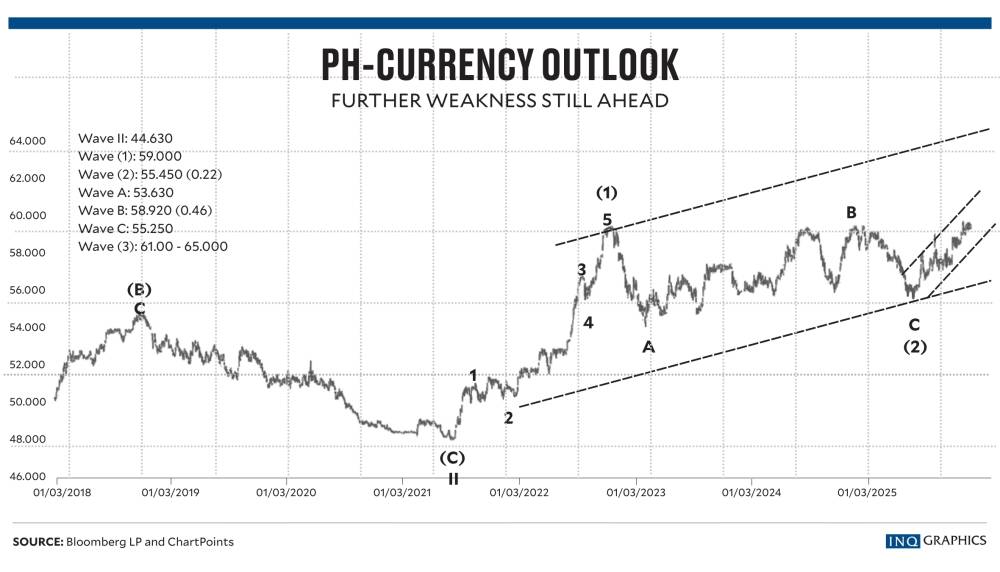

PHP outlook: 2026 to 2028 amid geopolitical and trade risks

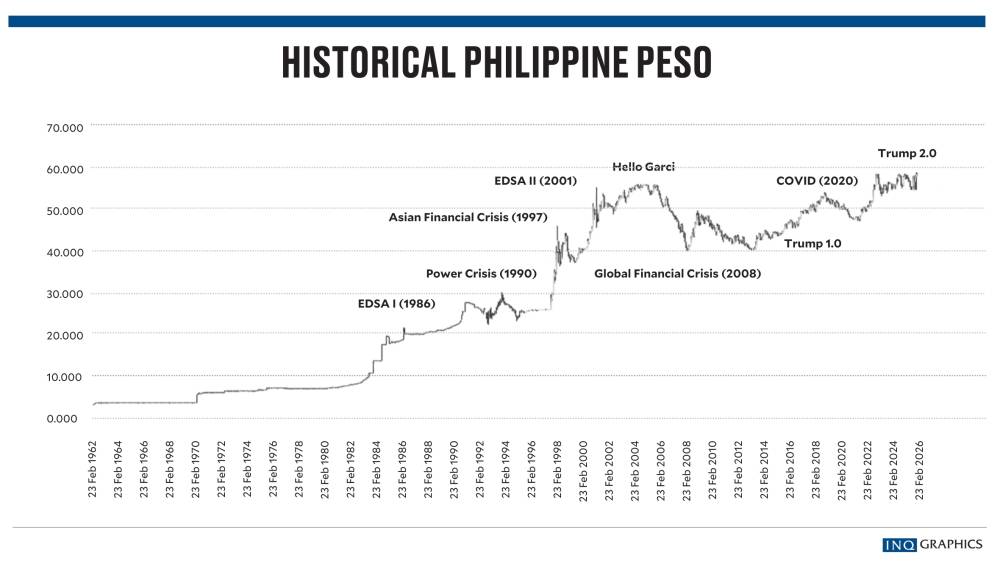

The Philippine peso enters 2026 on a relatively stable footing, trading near P58.90 per USD after its 2022 peak of P59.

Key fundamentals remain supportive: the Bangko Sentral ng Pilipinas (BSP) expects inflation to stay within the 3- to 3.5-percent band, aided by tariff cuts on rice and easing global oil prices.

Economic growth is projected at 4.5 to 5 percent, driven by infrastructure spending and resilient remittances, which account for roughly 10 percent of GDP.

Additionally, the BSP’s over $100 billion in foreign exchange reserves provide a significant buffer against short-term volatility.

However, structural vulnerabilities persist.

Consensus forecasts point to a mild depreciation trend: P58 to P61.30 in 2026 (average P60.100), P61.50 to P62.60 in 2027, and potentially P63.80 by mid-2028 before easing to P61.30 by year-end.

External risks dominate this outlook. Trump-era tariffs could squeeze margins for electronics and business process outsourcing exports, widening the trade deficit.

Rising geopolitical tensions, particularly in the West Philippine Sea, threaten FDI inflows, while stalled energy projects at Reed Bank sustain import dependence.

Lost fisheries alone could cost an estimated P1.3 billion annually.

Despite these positive fundamentals and the BSP’s effectiveness in managing currency volatility, the peso remains vulnerable to external shocks.

Scenario analysis suggests a base case of P60 to P62 by 2028, a bear case of P64 to P65 under severe geopolitical escalation and a bull case below P58 if tariffs are rolled back and FDIs surge.

In short, while strong reserves and remittances provide cushions, global trade frictions and regional security risks will continue to weigh on the currency’s long-term trajectory.

Geopolitical overlay: The currency risk multiplier

Politics now matters more than ever for currency markets.

The Russia-Ukraine war sustains commodity volatility, favoring resource exporters but straining net importers like the Philippines.

The Israel-Hamas conflict disrupts Red Sea shipping lanes, inflating freight costs and adding 0.5 percent to global inflation.

Brewing tensions in Central Asia threaten energy supply chains, accelerating friend-shoring and trade fragmentation.

Meanwhile, the West Philippine Sea dispute imposes tangible economic costs beyond sovereignty concerns— lost fisheries, delayed energy projects and heightened security spending erode current account buffers—amplifying peso risk.

These geopolitical flashpoints reinforce dollar hedging behavior globally, even as some nations experiment with alternatives.

Strategic implications for businesses and investors

For corporates and portfolio managers, the message is clear: resilience requires proactive currency risk management.

Diversifying exposure beyond the USD—into CNY, SGD and hedging instruments—should be a priority.

Scenario planning is essential: stress-test for USD or PHP at P65 under worst-case geopolitical escalation. Leverage Asean’s pivot to intraregional trade to hedge against tariff shocks. Monitor BSP policy signals closely; its stance on rate cuts and reserve deployment will be critical in anchoring peso stability.

Finally, businesses should embed geopolitical risk into treasury operations, as currency volatility increasingly reflects political rather than purely macroeconomic fundamentals.

Dollar dominance prevails, but prepare for a multicurrency future

Reports of the dollar’s demise are greatly exaggerated.

Structural advantages—such as deep liquidity, institutional trust and global network effects—ensure its supremacy for at least another decade.

Yet incremental erosion is inevitable as geopolitical fragmentation, technological innovation and regional integration reshape global finance. For Asean, and the Philippines in particular, the interplay of tariffs, geopolitics and structural reforms will dictate currency paths more than traditional macro drivers.

Expect moderate peso depreciation to P60 to P63 by 2028, with tail risks skewed to the downside.

Businesses that anticipate these shifts through diversification, hedging and strategic agility will be best positioned to thrive in an era of currency realignment.

(The author is one of the Philippines’ most respected analysts and market strategists. He is senior adviser at Reyes Tacandong & Co., and independent director at PH Resorts Group Holdings Inc. and DITO CME. For over 20 years, he was chief market strategist at BDO Unibank. A certified technical analyst, he combines data-driven precision with strategic foresight, making him a trusted voice in Southeast Asia and global economic fora.)