Stock picks: A mix of defensive, pro-cyclical companies

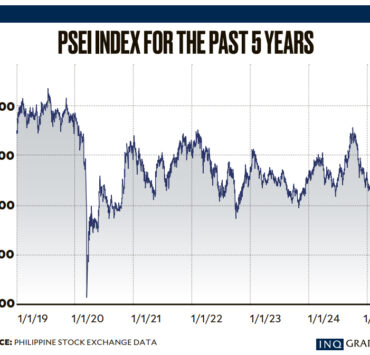

Cheers erupted when US President Donald Trump hit the pause button on his “Liberation Day” tariffs, and the local bourse has since been struggling to climb.

But as external threats loom, analysts surveyed by the Inquirer are encouraging traders to bet on defensive industries unaffected by the economic climate, including companies that offer high dividends like real estate investment trusts.

Others see strength in emerging sectors that have the potential to debut on the 30-member Philippine Stock Exchange Index (PSEi) by its next rebalancing in August.

For some, banks are still the strongest players, especially since these are again expected to report the most favorable earnings.

Here are their top three stock picks for the next 12 months.

Ron Acoba Chief investment strategist, Trading Edge Consultancy

1. Apex Mining Co. Inc. (APX)

“APX will continue to benefit from the rise in gold. At current price, APX is still trading at a single PE of 8.6x. Gold will continue to rise on the back of the ongoing uncertainties in the global market and the likely cut in Fed rates later on.”

2. DigiPlus Interactive Corp. (PLUS)

“PLUS is only trading at 14x price to earnings (P/E). It should trade at least 20x given its explosive earnings growth. Moreover, it will most likely be included in the PSEi in August.”

3. BDO Unibank (BDO)

“Banks will rerate higher given the recent reserve requirement ratio and interest rate cuts by the Bangko Sentral ng Pilipinas (BSP).”

Rastine Mercado Research director, Chinabank Securities

1. BDO Unibank

“We think that banks could continue to be attractive, especially given the outlook for sustained credit demand growth from corporates and consumers. Specific to BDO, we think that its scale will continue to provide an advantage, while its strong coverage levels provide a buffer against possible asset quality risks amid heightened external uncertainties.”

2. Citicore Energy REIT Corp. (CREIT)

“We think that REITs will remain attractive in that they are able to provide better stability through regular dividend payments. We think that CREIT’s stable portfolio, the essential nature of its tenants’ business of power generation, and its attractive dividend yield makes it a good addition to an investor’s portfolio. Moreover, the outlook for a growing portfolio to support its sponsor’s development plan could further provide windfall to dividends.”

3. Aboitiz Power Corp. (AP)

“We also like AP given the outlook for stable demand in its distribution business and additional capacity coming online in its power generation business this year. We think its recent pullback following its dividend payment also provides an opportunity for entry—especially as its prospective dividend yield remains attractive as well.”

Wendy Estacio-Cruz Research head, Unicapital Securities Inc.

1. Bank of the Philippine Islands (BPI)

“BPI’s premium over its peers is warranted as we expect the bank to sustain high return on equity levels amid strong earnings growth.”

2. Puregold Price Club Inc. (PGOLD)

“It is less likely to be affected by ongoing tariff headwinds and undemanding valuation.”

3. Converge Information and Communications Technology Solutions Inc. (CNVRG)

“It is expected to post higher-than-peers’ earnings per share growth of 6 percent, underpinned by an expanding addressable market and increasing adoption of prepaid fiber.”

Nicole Aquino Analyst, First Metro Securities

“We prefer consumer and property names poised to benefit from improving macroeconomic backdrop marked by disinflation and monetary policy easing, with domestic earnings drivers mitigating the direct impacts of Trump 2.0 policies. In this context, we highlight stocks with strong positioning and proactive strategies to capture growth opportunities across their respective segments.”

1. Ayala Land Inc. (ALI)

“Despite challenges in the Philippine property sector, we maintain a constructive view on ALI with target price at P35.80, reiterating our positive outlook. We expect earnings to remain resilient, supported by management’s ability to adapt to market headwinds. In the property development segment, pre-sales are likely to pick up in 2025, driven by back-ended launches in December 2024 and lower mortgage rates.”

“Additionally, the pickup in commercial and industrial lot sales is expected to contribute to earnings growth moving forward. Office leasing revenue to grow at a stable pace, supported by steady to improving vacancy rates and higher rents, while mall revenues are also expected to accelerate into 2026 as renovations gain traction, with core malls scheduled to reopen in second quarter 2025.”

2. SM Prime Holdings Inc. (SMPH)

“We remain positive on SMPH, with a target price of P32, as it is the best-in-class among Philippine mall operators, backed by strong branding and a gross floor area (GFA) of over 9.6 million square meters, representing about 50 percent of total mall GFA nationwide. When valued on its own using a 6.5-percent to 9-percent capitalization rate on P66.1 billion in mall earnings before interest, taxes, depreciation and amortization, we estimate the segment’s value to be between P734 billion and P1.016 trillion—above SMPH’s current market capitalization of P632 billion.”

“Investor concerns such as residential oversupply, high office vacancy rates and elevated reclamation costs are already factored into our forecasts, and improvements in these areas could present potential upside. To address these, the company plans to target the high-end residential market and ramp up provincial launches. For its office segment, the company is capitalizing on the strong demand for its mall-based offices and expanding into provincial markets.”

3. Puregold Price Club Inc.

“PGOLD is set to benefit from favorable macroeconomic conditions in the Philippines, with a target price of P36, with consumer spending recovering as seen in its strong fourth quarter 2024 results. Easing inflation, which dropped to 2.6 percent from 4.3 percent in the same period last year, and improving consumer sentiment, as indicated by the [BSP’s] latest survey, are key drivers of this growth. These trends benefit PGOLD, given its focus on low- to middle-income households whose spending is sensitive to inflation. Additionally, the company’s margins remain well supported, as it did not need to cut prices in fourth quarter due to higher consumer spending power. Moreover, the appreciation of the Philippine peso against the US dollar is expected to support S&R’s margins, given the business’ reliance on imported products.”

Alfred Benjamin Garcia Research head, AP Securities Inc.

“Our top picks this year are companies that can weather economic downturns and primarily focus on domestic demand.”

1. Converge ICT Solutions

“CNVRG has now entered the next leg of its growth story as it reaps the fruits of its investments in expanding its business.”

2. Puregold Price Club

“PGOLD is another top pick, as demand for consumer staples should pick up this year against the backdrop of benign inflation and rising real wages.”

3. Metropolitan Bank & Trust (MBT)

“MBT is the bank that is in the best position to benefit from the expected increase in demand for corporate loans as rates start to come down in earnest. The bank’s conservative approach to lending and its generous dividend policy also makes it a good defensive play.”