A look at 2025 condo sales trends

Metro Manila’s residential condo market in 2025 is navigating a complex environment shaped by tempered demand, persistent oversupply, and structural shifts in buyer behavior.

While sales activity remains steady, the forces driving acquisition decisions are evolving, particularly among investors who are reassessing options in terms of returns. There are two general reasons for buying property: one is for end-use and the other is for investment.

While end-users as a source of demand can be multi-faceted in their considerations—be it emotional, practical, or other reasons—investors focus more on returns.

Demand drivers hold, but investor confidence remains soft

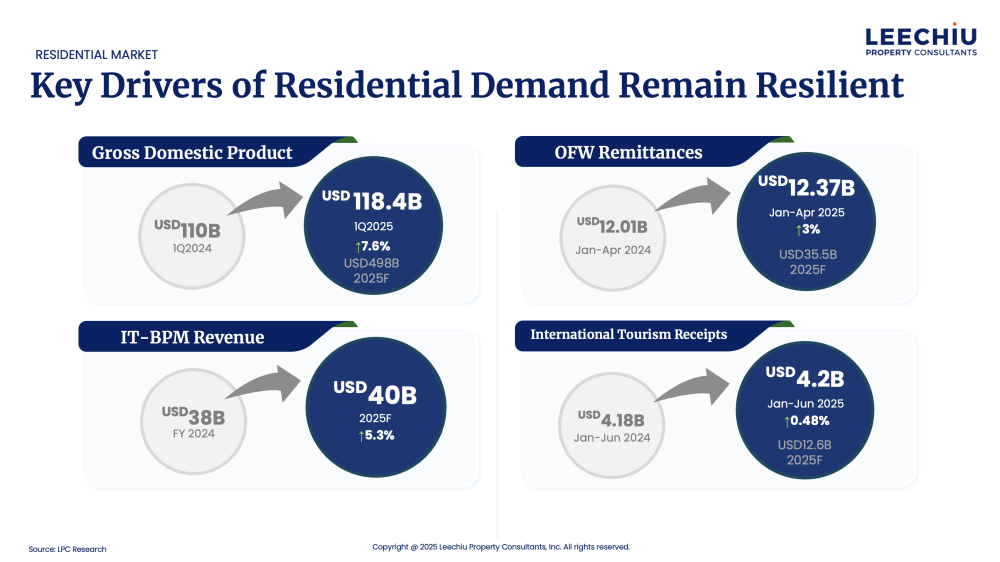

The market continues to benefit from stable demand fundamentals.

The Philippine economy grew by 7.6 percent year-on-year, OFW remittances rose by 3 percent in the first four months of 2025, and tourism revenues increased slightly by 0.48 percent YOY.

However, property demand has not picked up at the same pace. Condominium take-up improved by only 2 percent from the previous quarter, while new launches rose by 31 percent, adding to the 82,800 unsold units across Metro Manila, equivalent to 37 months of supply.

This exists alongside the national housing backlog estimated at 10 million units, underscoring the disconnect between available inventory and actual housing needs.

Investor sentiment remains cautious, shaped by evolving market conditions and shifting rental dynamics.

In areas like Bay Area, leasing activity has yet to fully recover, prompting investors to take a more measured approach.

While developers are offering more flexible payment terms and attractive financing, many buyers are prioritizing long term value and income stability. This has contributed to more selective investment behavior, influenced by market absorption and future returns.

Structural headwinds and cautious buying behavior

The market is still adjusting to structural shifts, including the exit of Philippine offshore gaming operators (Pogos), which disrupted leasing demand in key areas such as the Bay Area and contributed to the prolonged softness in rental rates.

The sector’s historical reliance on external demand drivers, including Pogo tenancy and OFW-driven acquisitions, has made it more susceptible to global disruptions and regulatory changes.

These factors have contributed to a more conservative approach to property purchases, especially among investment-oriented buyers.

Pricing trends and perception gaps

Primary condo prices have seen increases in several locations, reflecting developers’ long term view of property values. However, these adjustments may not always align with near term market sentiment.

With unsold inventory rising and leasing activity still recovering, price resistance is becoming more common, particularly among buyers who are watching for better value or more favorable entry points.

The condominium supply level and pace of rental recovery have contributed to a

disconnect between pricing expectations and buyer confidence. A more market-responsive approach may help sustain interest and support stronger transaction activity in the coming quarters.

What buyers are looking for

Today’s buyers are pragmatic and risk-aware. End-users continue to gravitate toward compact, functional units in the mid-market segment, while investors are targeting projects with stronger leasing fundamentals and pricing headroom.

Larger and high-end units saw mixed performance, and speculative interest remains muted.

To support sales, some developers introduced incentives such as rent-to-own schemes, longer payment terms, and stronger after-sales service. Financing institutions and Pag-IBIG have also rolled out reduced rates and extended amortization options that help improve affordability.

Still, investors remain observant of market signals and are taking a more gradual approach as they monitor improvements in leasing activity and unit take-up.

Rebuilding confidence through value and support

In a market challenged by oversupply and modest rental performance, the relationship between developers and buyers must shift toward long term value creation. Beyond price-based incentives, developers are encouraged to offer risk-reducing and income-enhancing measures, such as rent support programs, tenant placement assistance, and ongoing property management.

These strategies can help rebuild confidence and encourage more sustained engagement from both end-users and investors, especially in segments where pricing and yields are still stabilizing.

The author is the director for Research, Consultancy, and Valuation at Leechiu Property Consultants Inc.