Closing the gap: The road to housing affordability

While housing is a basic need, owning a home remains an aspirational goal for many Filipinos—a symbol of success, stability, and security.

Yet, achieving it has become increasingly difficult given today’s property prices and lagging income growth. Can the typical young Filipino family today ever own a home?

From boom to imbalance

In Metro Manila, residential condominiums have been part of the Philippine real estate landscape for over five decades. Their popularity surged in the early 2000s as the country evolved into a hub for Information Technology and business process management (IT-BPM) jobs.

Real estate developers seeing the rise of employment responded with a wave of high-rise projects across the National Capital Region (NCR). Add to the overseas Filipinos (OFs) fueling demand for residential units, as they invest in properties for family use or as income-generating assets while working abroad.

Further pushing demand higher was entry of Philippine offshore gaming operators (Pogos), which distorted demand and pricing. The premium rents the Pogo sector was willing to pay attracted speculative investors who raised demand levels, so developers built even more units.

The real estate industry saw its peaks in demand for the office and residential sectors in 2018 and 2019, just before the pandemic hit.

Today, a year after Pogos left the market, demand for small condominium units have declined.

As of November 2025, Metro Manila has 80,300 unsold condominium units. Most of this oversupply sits in the upper middle (P4 million to P7 million) and upscale (P7 million to P12 million) segments, accounting for 32 percent and 35 percent of unsold stock.

All this while there is barely any new supply in the low-income segment, with less than 1 percent of remaining supply.

The bigger picture

Zoom out and the issue of lack of supply and mismatch in price affordability becomes even more apparent.

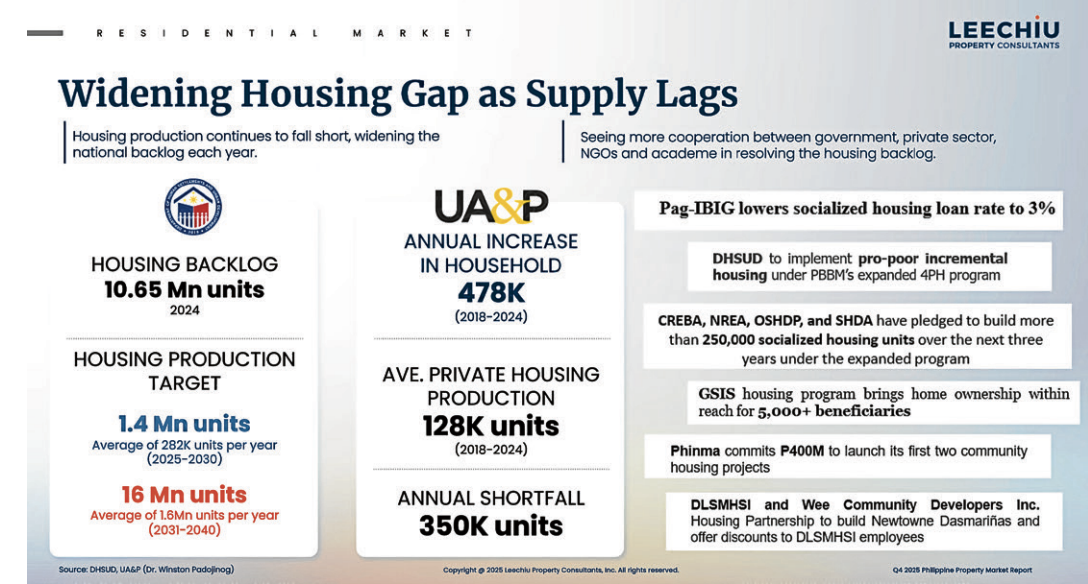

The Department of Human Settlements and Urban Development (DHSUD) reported that the national housing backlog hit 10.65 million units in 2024 and will balloon further unless production accelerates in underserved segments.

Dr. Winston Padojinog of the University of Asia & Pacific and its esteemed think tank, the Center for Research and Communication, estimates that the average annual new home demand is about 478,000 units (average of 2018 to 2024), while only 128,000 housing units are produced by the private sector for the same period.

This, unfortunately, results in an annual shortfall of 350,000 housing units. Closing the gap requires 282,000 units to be produced yearly from 2025 to 2030, and a staggering 1.6 million units annually from 2031 to 2040.

The affordability gap

Data from the Philippine Statistics Authority show that household incomes in NCR grew by only 20 percent since 2019, while residential property prices surged 62 percent, according to the Bangko Sentral ng Pilipinas (BSP) Residential Property Price Index.

This mismatch isn’t unique to the Philippines. Countries like the US, Australia, and Singapore face similar challenges. But here, the impact is harsher because incomes start from a much lower base.

Public-private collaboration in action

The urgency of the housing issue was the main topic at an event, titled “Mind the Gap: Housing Affordability in the Philippines”, held in November last year.

Industry leaders discussed difficulties in the permitting processes as well as the need for long-term strategies to effectively address the housing backlog and for adjustments in the current price ceilings for mass housing, among other issues. Pag-IBIG Fund also announced that it offers developmental loans to support housing initiatives, underscoring the role of funding in bridging the gap.

The discussion made clear that while public and private sectors are taking steps, structural issues—such as pricing, policy frameworks, and regulatory bottlenecks—remain major hurdles to accelerating affordable housing delivery.

DHSUD echoed this collaborative stance. In July, DHSUD Secretary Jose Ramon Aliling said: “Private stakeholders are more willing to engage when there is clarity and fairness in government programs.”

Policy shifts and emerging models

Stakeholders are moving to address the gap.

Policy reform discussions among government, private sector, and academe focus on adjusting price ceilings and compliance frameworks. DHSUD recently raised the ceiling for socialized housing to P950,000 for house-and-lot units and P1.8 million for condominiums, aiming to attract developers to segments where demand is greatest.

The expanded 4PH program now includes rental housing options—ideal for families needing secure homes without committing to a purchase. Alternative models like rent-to-own schemes are gaining traction, signaling a shift toward flexibility and inclusivity.

Building communities

Urban housing models are evolving. Developers are creating integrated communities with schools, hospitals, and retail hubs—housing is more than just putting roofs over heads, it’s about ecosystems where families can thrive.

When families live closer to work, productivity rises, commutes shorten, and cities become more livable. The solution isn’t just more units—it’s financing, infrastructure, and policies that make affordable housing viable for developers and realistic for buyers.

The real question

The gap is there and narrowing this gap can be done—but should be seen as a long-term effort involving systemic change.

If government agencies, developers, and financial institutions pull in the same direction, this crisis can become a positive turning point. The question isn’t whether we can build more homes—it’s whether we can build the right homes, in the right places, at prices people can afford.

The author is the director for Research, Consultancy, and Valuation at Leechiu Property Consultants