House & Lot is hot: End-users reshape the resi plot

The Philippine residential market is undergoing a decisive shift–one that increasingly favors space, scale, and suburban living.

I have consistently highlighted the sustained strength of house-and-lot developments, driven largely by end-users rather than speculative investors. In the post-pandemic environment, we at Colliers Philippines have seen more Filipino buyers prioritizing larger homes, greener environments, and greater access to integrated communities.

This demand has naturally redirected developer attention to growth corridors outside Metro Manila, particularly Calabarzon Region.

Improved infrastructure connectivity, coupled with rising purchasing power of households, is unlocking the potential of the region and enabling the rise of masterplanned townships that blend residential, commercial, and lifestyle components.

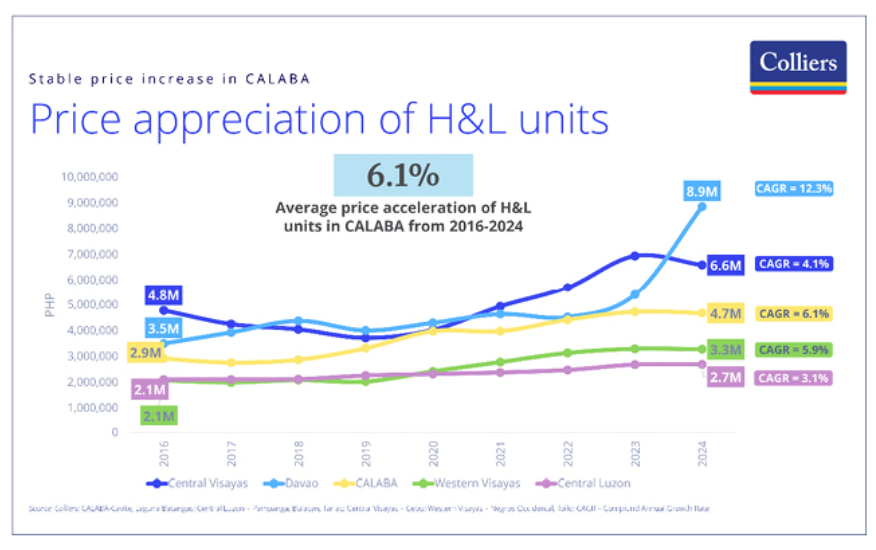

Notably, horizontal projects continue to demonstrate pricing resilience. House-and-lot (H&L) developments, especially in Southern Luzon, have posted steady appreciation, supported by robust end-user demand, remittance inflows, and broader economic expansion.

Rethinking development pipelines

As I mentioned in my previous pieces, the pandemic compelled landlords to rethink their massive office and condominium development pipelines. Such plans were shelved as demand for these buildings substantially slowed especially from 2020 to 2021.

There’s no doubt that developers are aggressively following where their buyers are investing. Property firms have been expanding outside the capital region to capture steady demand in primary residential investment hubs including South Luzon.

The horizontal market’s upside potential

Colliers has observed steady demand for horizontal projects, particularly H&L developments. We encourage developers to consider viable locations for H&L and lot-only projects including provinces in Calabarzon.

H&L developments remain popular especially in the provinces due to the availability of affordable units given the relatively cheaper developable land. Most overseas Filipino workers (OFWs) from the provinces also prefer a larger space for their families.

Overall, the H&L market, particularly in major urban areas outside the capital, should be propelled by sustained growth in remittances, a portion of which will continue to finance the amortization of the OFWs’ properties, as owning a house is every Filipino’s aspiration.

In Luzon, the Cavite-Laguna-Batangas (Calaba) corridor accounts for the largest stock of H&L units, with more than 360,000 units posting an absorption of 92 percent as of end 2025.

From 2016 to 2024, prices of H&L units in Cavite, Laguna, and Batangas increased by an average of 6 percent annually. Average total contract price of H&L projects in Calaba stood at P3.5 million in 2025. The most expensive units are priced from P20 million to P43 million. These projects boast of impressive take-ups of between 40 and 100 percent.

Overall, Colliers Philippines believes that developers will continue to build residential projects in second- and third-tier cities and municipalities, where demand comes from local end-users, as well as those based in Manila, but are looking to buy in their home provinces as second homes.

The markets may be smaller compared to Metro Manila but are more stable in terms of end-user housing demand.