PH economy, real estate on the upswing

The Philippine real estate industry is still in a challenging environment because of local economic headwinds such as the persistently high inflation and higher-for-longer policy interest rates, geopolitical conflicts affecting the global economy, and the tail-end effects of the COVID-19 pandemic. This has resulted in a slower-than-expected recovery in the first half of 2024.

Positive prospects

Second half prospects, however, are positive given a surprisingly resilient economy and the noted positive movements in transaction volume year-on-year (YoY) across the real estate industry.

The expected decrease in policy interest rates in the last quarter of the year, as inflation is projected to stay within the target range of 2 to 4 percent, will further help in the industry’s recovery.

Last year, the Philippines registered the highest gross domestic product (GDP) growth in the Asean at 5.6 percent. Will this above-expectation performance continue in 2024?

Mc-Kinsey and Company presented three possible economic scenarios for the Philippines in 2024: slower growth, soft landing, or another year of accelerated growth.

Based on the first quarter economic performance and recent economic trends as of May 2024, the country is poised to have another good year economically, with GDP projected by the International Monetary Fund (IMF) to be at 6.1 percent, inflation contained under 4 percent as projected by the Bangko Sentral ng Pilipinas (BSP), and policy interest rates to decrease as early as Q3 2024.

All these factors will have a positive impact on the real estate market.

Additional economic indicators, such as employment rate, remittances from overseas Filipino workers (OFWs), GDP from construction, real estate loans, building permits, and the overall real estate contribution to GDP are all trending upward, providing the industry the needed conditions for a sustained recovery.

Vacancies, rents

Office vacancy rate stands at 18 percent, while rents have declined by 12.3 percent YoY, to P990 per sqm from P1,130 per sqm.

The softening in rent is a logical impact of having 2.3 million sqm of unleased or vacant office space and the 1.5 million sqm additional supply scheduled to be completed from 2024 to 2028.

Initially, the 1.5 million sqm pipeline supply may be unreasonable given the high vacancy rate in NCR.

However, a per city vacancy rate and pipeline supply analysis will reveal that developers are keenly aware of the situation and have started to rationalize the construction of new supply.

For instance, Parañaque and Bay City’s 41 percent and 28 percent vacancy rates, translated to a lower pipeline supply of 5 and 7 percent, respectively.

We have also noted that the decline in rental rates is correlated to the current vacancy rates.

As an example, Bay City and Alabang’s high vacancy rates of 28 percent and 32 percent, respectively, have resulted in substantial declines of 30.4 percent and 10.7 percent in average rents YoY. Makati’s 13 percent vacancy rate, meanwhile, resulted in a more manageable rental decline of 4.5 to 10.7 percent.

Sources of office demand

The business process outsourcing (BPO) industry is expected to continue its growth trajectory and will require close to 400,000 additional FTEs. This translates to a demand of 1.2 million sqm of office space for the next four years, half of which will be in Metro Manila.

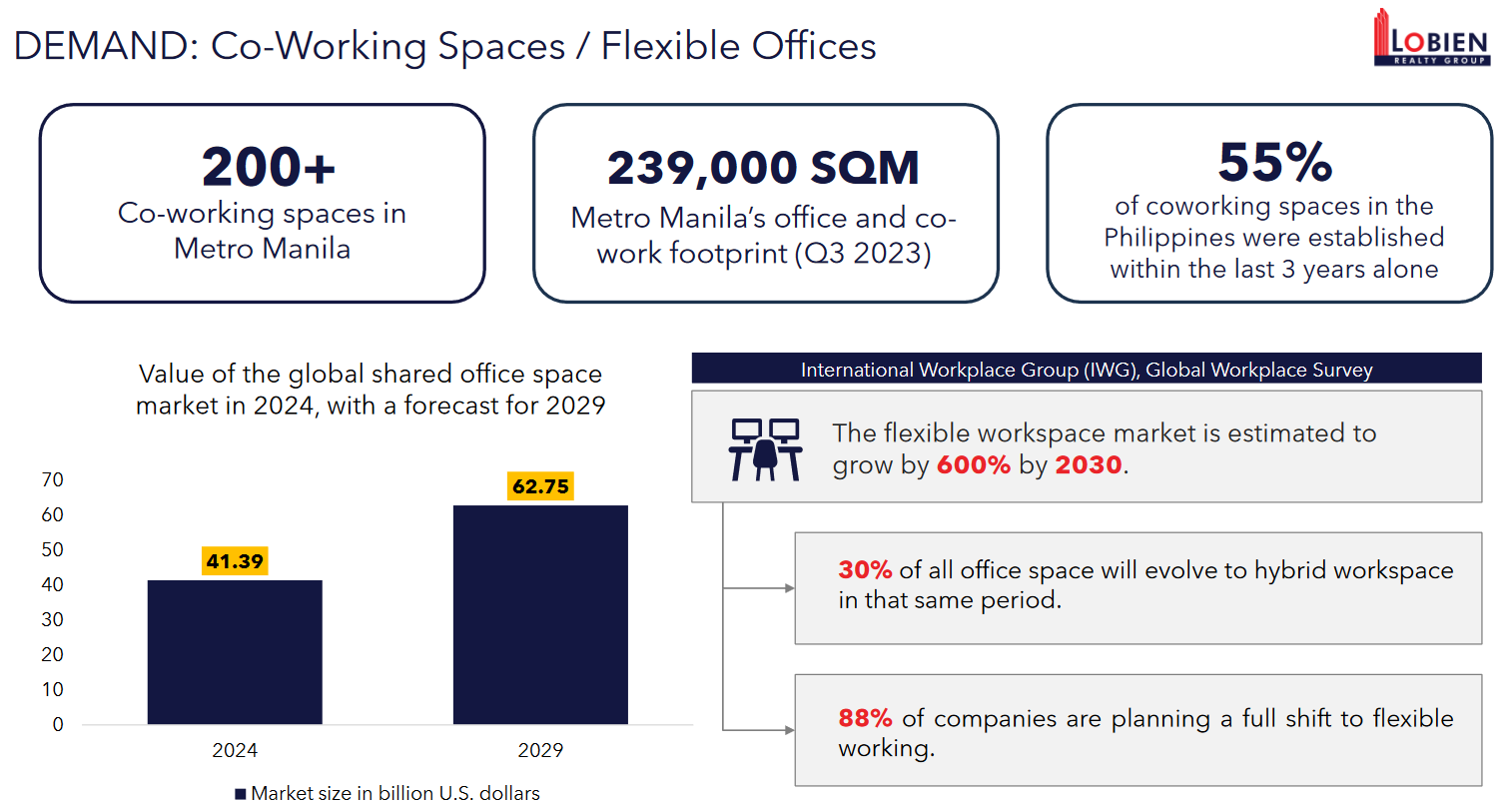

The co-working space, or flexible office industry, is another source of office demand. It will be part of the office space strategy of BPOs and traditional companies in terms of their business continuity, natural growth, and investment risk management strategies.

More than 240,000 sqm are currently being occupied by flexible office companies and more than 100 co-working offices have put up shop in the Philippines in the past three years. We expect this trend to continue, although at a slower pace, over the next three years.

Locators and tenants should therefore maximize the current high vacancy rate in the office space sub-market to secure their preferred locations and buildings at the best possible price, as there has been a noted increase of 100,000 sqm in office space take-up YoY. Only 18,200 sqm was leased out of the available supply in 2023 but this increased to 118,400 sqm as of Q2 2024, reflecting the possible start of the office market’s recovery in Metro Manila.

Residential spaces

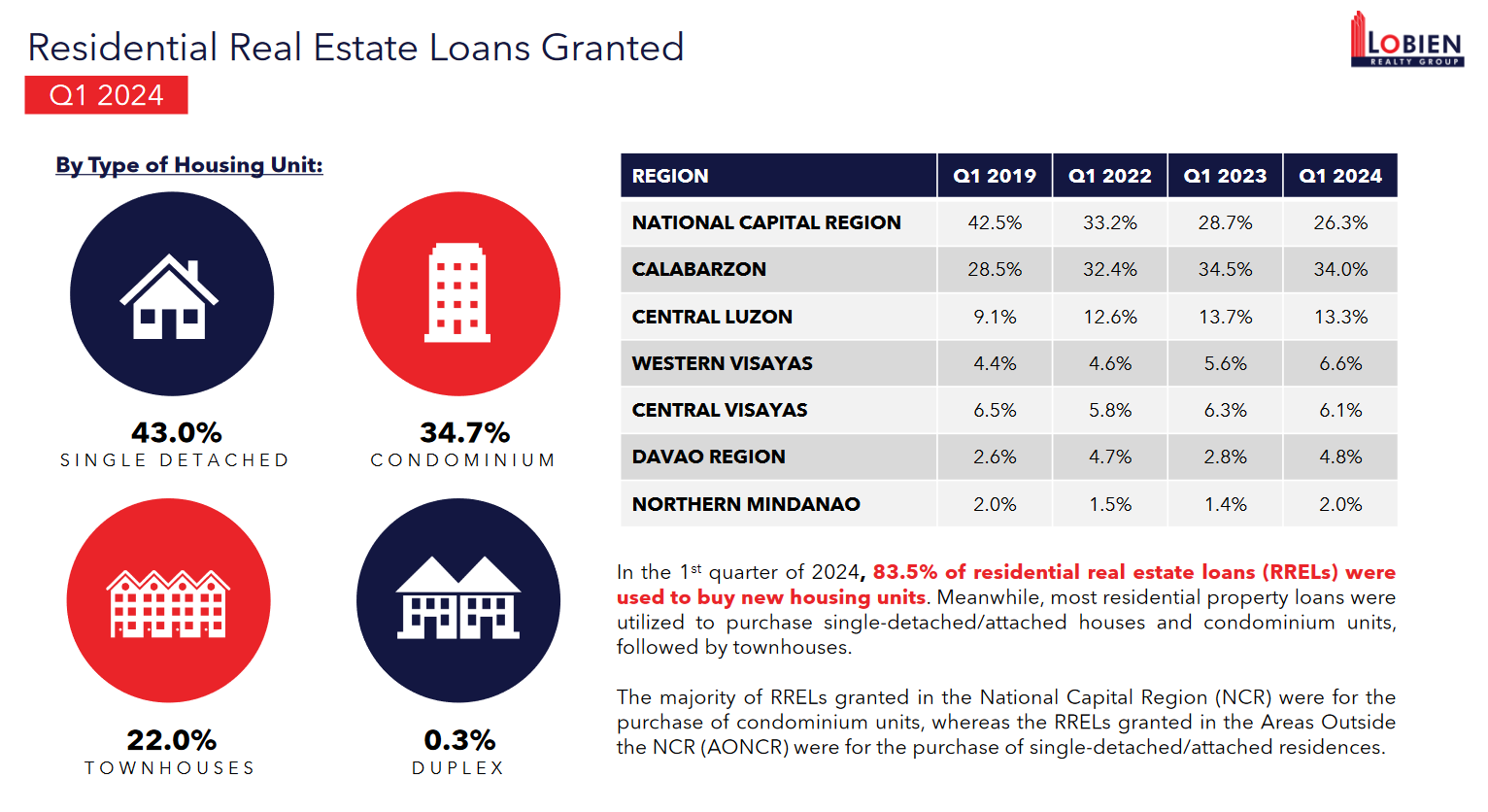

Around 10,000 residential condominium units will be added in 2024. Demand is robust, as reflected in the upward trajectory of residential prices based on the Bangko Sentral ng Pilipinas’ Residential Real Estate Price Index (BSP RREPI) as of Q1 2024. Condominium units registered the highest price increase at 10.2 percent while prices for all house types across the country increased by 6.1 percent.

On the demand side, a significant shift from NCR to Calabarzon Region can be noted based on the residential or housing loan data. Prior to the pandemic and until 2021, two out of every five loans (42 percent) approved by financial institutions were in NCR. This, however, steadily decreased to 33 percent in 2022, 29 percent in 2023, and 26 percent as of Q1 2024.

During this time, Calabarzon’s percentage share steadily increased from 28 percent to 34 percent. The increased preference for Calabarzon as a residential destination can be attributed to the strict lockdowns experienced in the NCR during the pandemic, the need for greater space for various family activities, the relatively lower price of residential units outside Metro Manila but with more space, and the increasing number of high quality estate and townships in the region.

However, we still expect the demand for mid to high end condominium market to remain, as their appeal to affluent customers and C-level executives to address their transportation and convenience requirements will remain. Thus, estate and townships within NCR are expected to be developed, and the market for this will continue to grow, providing further boosts to office, retail, and residential submarkets.

The author is the chief executive officer of Lobien Realty Group Inc., a full service real estate consultancy and property investments strategy firm